Retirement should be a time of clarity, not confusion over taxes. Every dollar you withdraw matters far more than the amount alone. The way you handle withdrawals can significantly affect how much you keep.

Here’s how to reduce taxes in retirement with simple yet powerful strategies.

Why Withdrawal Strategy Matters

Taxes can chip away at your retirement income. Withdraw too much too soon, and you might push into a higher tax bracket. Do not get caught paying more just because you missed the right timing.

A smart withdrawal plan helps you:

- Keep yourself in lower tax brackets

- Protect Social Security benefits from becoming taxable

- Preserve more of your nest egg for longer

- Reduce the risk of sudden tax burdens when you least expect them

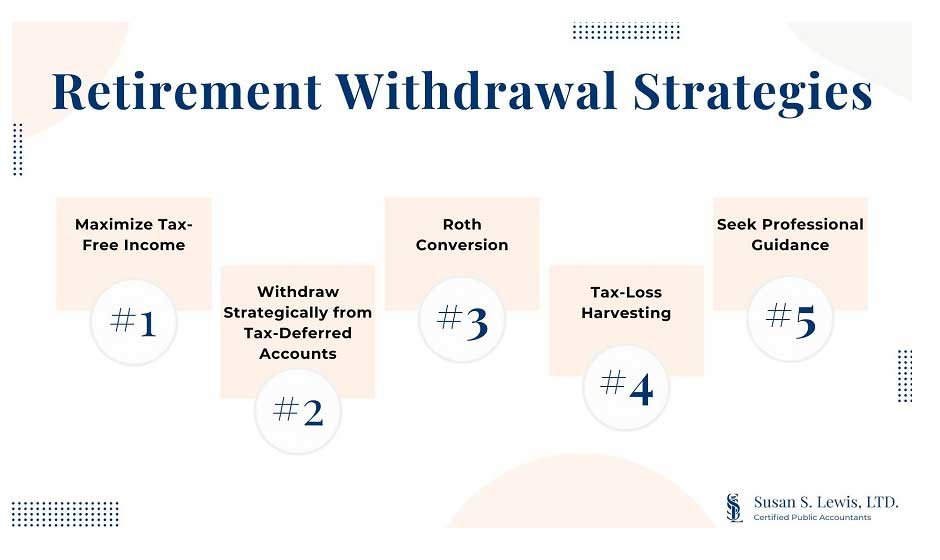

Winning Withdrawal Tactics

1. Withdraw from Taxable Accounts First

Tap into taxable accounts first, before withdrawing from IRAs or 401(k)s. This gives your tax-deferred accounts time to grow without triggering immediate tax on growth.

2. Spread Out IRA Withdrawals

Taking large sums from IRAs in one year risks pushing you into a higher bracket. Instead, withdraw smaller amounts over several years. It helps manage your tax burden calmly and wisely.

3. Use Roth Conversions Strategically

If you think your tax rate is lower now than it will be in future, convert some of your tax-deferred funds to Roth. You pay tax now, but future withdrawals are tax-free. It may cost less in the long run.

4. Watch Your Social Security Income

A portion of your Social Security may become taxable if your “combined income” exceeds certain thresholds. By planning withdrawals carefully, you avoid unexpected taxes on benefits you rely on.

5. Minimize Required Minimum Distributions (RMDs)

IRAs and 401(k)s require you to withdraw at least a minimum amount each year after you reach a certain age. Ignoring this can result in steep penalties or higher taxes. Plan RMDs ahead, so they don’t disrupt your income strategy.

Real-World Example

Consider Joan, a retired teacher. She started with a large IRA and no Roth savings. At 72, she faced big RMDs that pushed her into a high tax bracket. Suddenly, taxes took more than expected from her income.

After working with an advisor, she shifted:

- First, she used her taxable accounts for income.

- Then, she converted some IRA funds to Roth yearly while her tax rate was lower.

- Social Security stayed mostly shielded from tax.

- RMDs became manageable.

As a result, she saved thousands each year—and kept her future income secure.

Common Mistakes to Avoid

- Waiting too long to convert to Roth. You may miss lower-tax opportunities early on.

- Unknown income triggers. Know thresholds for Social Security taxation and Medicare premiums.

- One-size-fits-all advice. Retirement plans must reflect your unique tax rates and sources of income.

- Going solo without perspective. Tax laws shift, markets change, your needs evolve.

Why Professional Guidance Helps

Retirement tax planning is not about chasing loopholes. It is about clarity and control. It requires discipline, strategy, and insight.

If you value peace of mind, consider trusted help. TruNorth Advisors can work with you to build a withdrawal strategy that preserves more of what you have saved.

Bottom Line

Taxes in retirement are not inevitable—painful they are not. With a plan that sequences your withdrawals wisely, you control how much the IRS takes.

Start with the right order. Space out your IRAs. Use Roth conversions with purpose. Shield your Social Security. And honor RMDs before they honor penalties.

With strategy that respects your future, your retirement income stays where it belongs—secure, comfortable, and tax-smart.